Only 30 days have passed since the beginning of 2025, but this is probably the tenth time you have heard that this is the year of VC in Italy—the latest news of foreign funds opening offices in Italy, the first rounds already announced, the recently published reports, everything seems to point in this direction.

In today’s article, we begin exploring who the key players making this possible could be, starting with Business Angels (BAs). Why start with them? Because as IAG, we have seen more than 550 angels join our network over our 17 years of activity… which has allowed us to closely analyze who they are, how and why they invest, and what impact they have on the ecosystem.

Ready? Let’s start with the basics: Who are Business Angels?

BAs are individuals with solid skills and experience, often former entrepreneurs, managers, or professionals, who invest their own capital in promising startups. Their contribution is not limited to capital: they offer mentorship and access to their network, becoming true strategic partners for startups, especially in the early stages (pre-seed and seed). They can act alone or through Business Angel Networks (BANs), such as Italian Angels for Growth (IAG), pooling their efforts and resources.

Being part of a BAN means accessing an ecosystem that offers selected opportunities, strategic support, and engagement with other investors. In recent years, BAs have evolved from independent figures into members of a collective system that creates an impact on the entrepreneurial ecosystem.

Finding the right investors is one of the most complex challenges for a founder. Having an innovative idea is not enough; it is also necessary to know where to look.

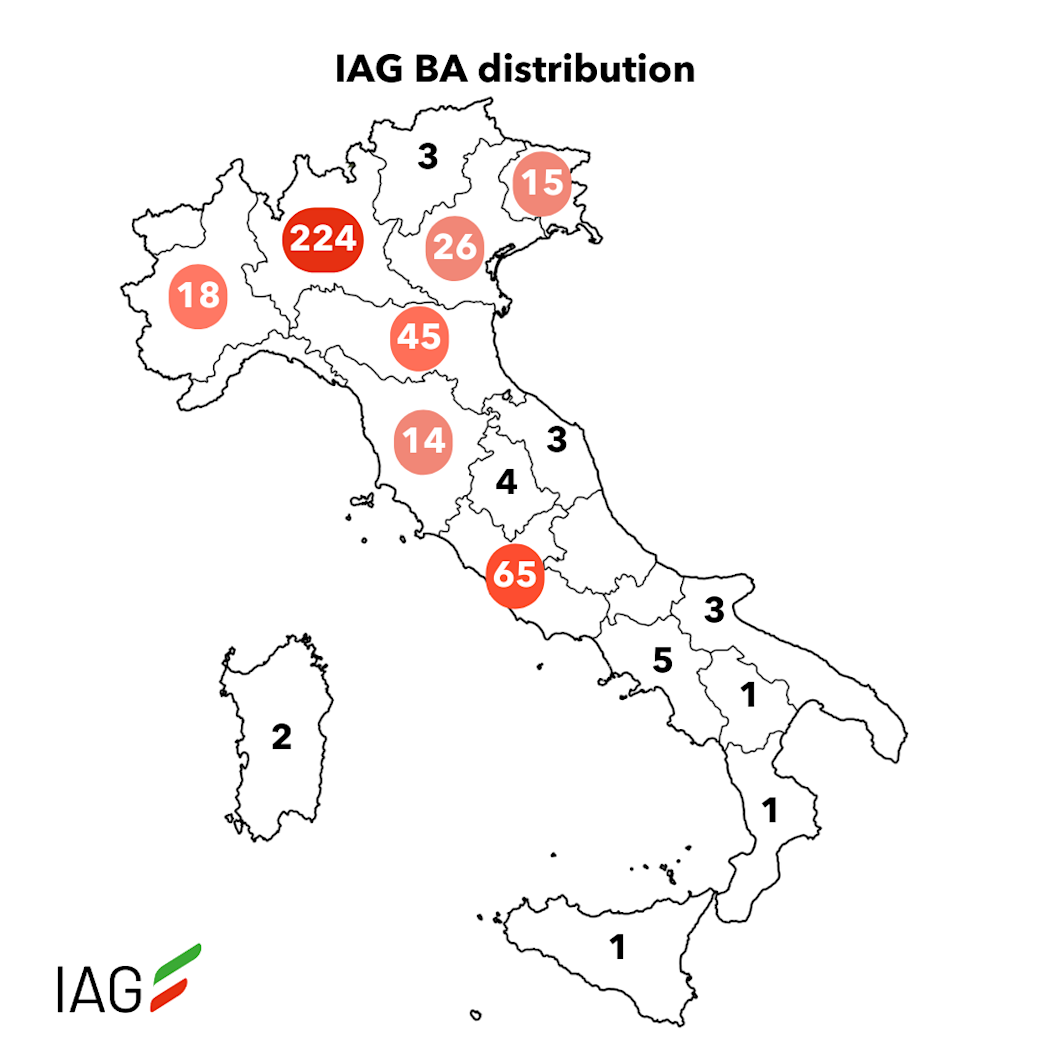

Analyzing the geographical origin of IAG members, a strong concentration in Northern Italy emerges, with Lombardy leading, followed by Lazio. This data reflects not only the distribution of wealth across the country but also the presence of more developed entrepreneurial and financial ecosystems in the northern regions. The gap with Southern Italy is significant and raises questions about the territorial dynamics of angel investing.

The scarcity of BAs in the South could be attributed to various factors: a lower density of innovative startups, less advanced technological infrastructure, and a historically less entrepreneurship-oriented tradition in high-growth sectors. This, in turn, fuels a vicious cycle. Fewer investors mean less capital available for local startups, further limiting the ecosystem’s development. However, it is interesting to note that some regions in the South are trying to reverse this trend through local initiatives and targeted acceleration programs that aim to close the gap in the coming years.

IAG BA distribution

IAG BA distributionStill haven't found your ideal BA? You can try filtering them by professional background.

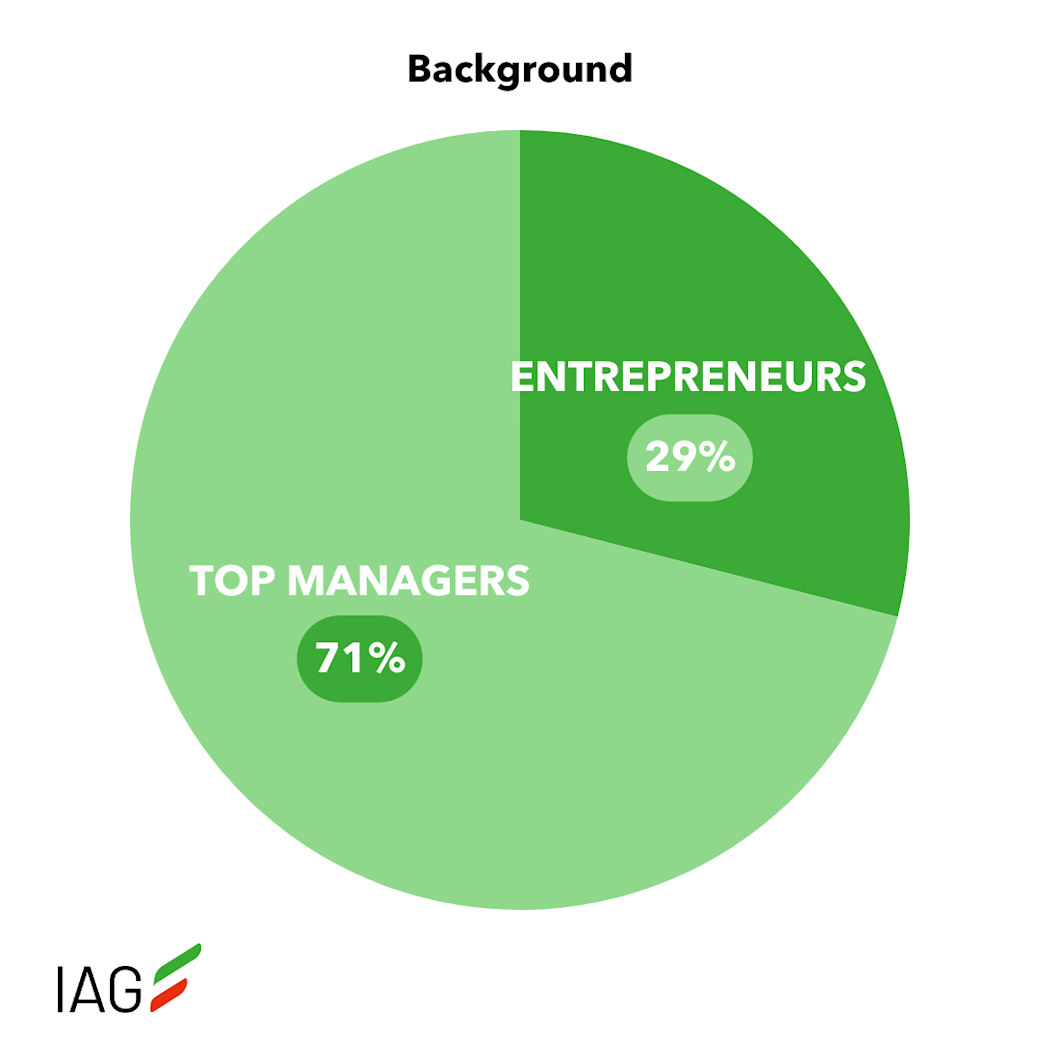

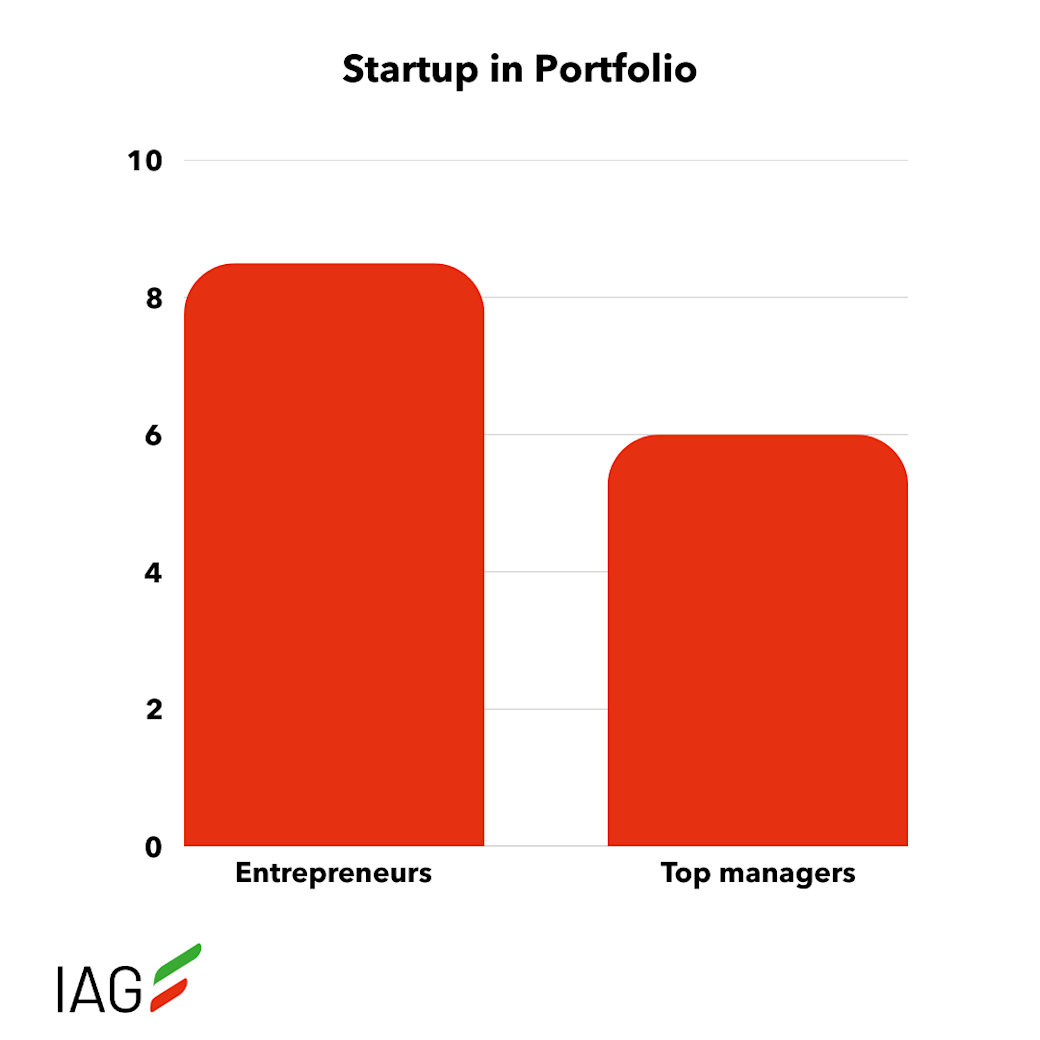

One of the most interesting aspects of analyzing the IAG network is the professional background of angel investors and how this influences their investment choices. Angels with an entrepreneurial background—including freelancers—make up about 29% of the total and, on average, have a larger portfolio of 8.74 startups. In contrast, the remaining 71%, mainly composed of top managers from large or medium-sized national and multinational companies (primarily C-level and directors), have an average of 5.67 startups in their portfolio.

Background

BackgroundThis difference can be explained in several ways. Entrepreneurs are often more inclined to take risks, having personally experienced the challenges and uncertainties of building a business. This mindset leads them to invest more capital in high-risk investment opportunities, such as venture capital. By doing so, they increase the number of investments and startups in their portfolio while also being more willing to invest in sectors they are less familiar with. Paradoxically, this allows them to diversify their portfolio more effectively than others, thereby reducing risk. Conversely, top managers of large companies, despite having solid management and leadership experience, may be more cautious in their investments due to a background that has accustomed them to operating in more structured and less uncertain environments.

Startup in Portfolio

Startup in PortfolioAnother factor to consider is the capital available for investments. Entrepreneurs, having often monetized their businesses or working as freelancers, may have more liquid resources to dedicate to angel investing than corporate managers, whose personal assets may be less liquid or diversified into other assets.

However, both groups bring unique value to the ecosystem: on the one hand, entrepreneurs can offer startups practical guidance and direct insight into the challenges of entrepreneurial life, while on the other hand, managers contribute strategic, scalability, and management expertise, as well as their industry network—key elements for later-stage growth. This complementarity is one of the most fascinating aspects of BANs, where a wide variety of backgrounds and expertise come together to support innovation.

Now, let’s imagine switching roles—put yourself in the shoes of an angel investor. What does being a BA entail, and what are their rights and responsibilities?

Being a BA involves various risks, but it is also highly rewarding. Learning when to step in and guide the founder, when to give them space, and above all, how to build a portfolio are essential skills that all BAs should deeply understand. Let’s take a look at the insights from our analysis.

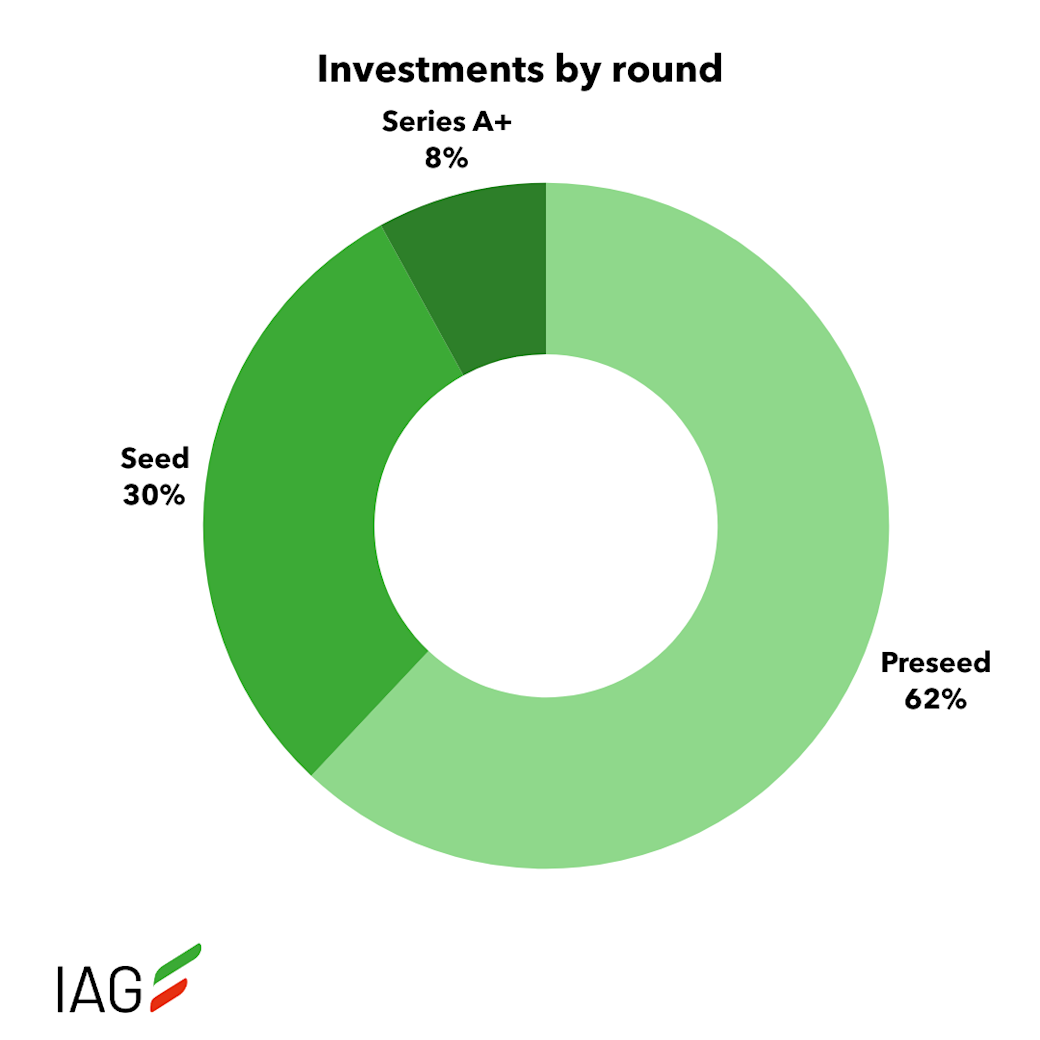

Over the 17 years of IAG’s existence, business angels have made 62% of their investments at the pre-seed stage, 30% at the seed stage, and only 8% in later stages.

Investments by round

Investments by roundBAs are often among the first “patrons” of a startup, providing not only capital but also expertise, network, and direct support during critical moments of vulnerability. However, there comes a time when other players, such as venture capitalists, must step in to support the business's growth and scalability.

Knowing when to “pass the baton” is one of the most complex yet crucial challenges for an angel. Continuing to support a startup through follow-on investments can signal trust and a willingness to strengthen the investment, which may make sense in certain cases. However, at the same time, it is important to maintain a balance and continue diversifying the portfolio with new opportunities. Blindly investing in follow-on rounds without a clear strategy or justification for the additional investment, while neglecting portfolio diversification, is a risk that some inexperienced angel investors overlook.

Speaking of diversification: the data mentioned earlier regarding the number of startups in our BAs’ portfolios tells an evolving story. Building a well-structured and diversified portfolio requires time, experience, and access to high-quality investment opportunities. Angels who choose to be part of IAG do so with this very goal in mind: to build an ideal portfolio, supported by an ecosystem that facilitates startup selection, provides networks and knowledge, and reduces individual effort. It is important to remember that there is no “perfect” number of investments; rather, the ideal strategy for each investor develops over time, with patience and attention.

The future of angel investing in Italy depends on this: the ability to create value in the early stages, the courage to make space for new players, the ability to find one’s individual investment strategy, and the vision of an increasingly mature and interconnected ecosystem.

That’s all for this month—see you next time and… happy investing!